Cool as a cucumber

That pineapple is way cooler. Coolest? A pile of tax free money thanks to a cash out refinance.

Who doesn’t love a pile of free money?

Imagine you won $26k in some sweepstakes. How excited would you be? So pumped! You immediately start dreaming up all the things you are going to buy… how much do those water jet packs cost?

Then your friend Debbie, who is always a downer, warns that you’ll have to pay taxes on the winnings. So you will really only receive $15k. Ouch.

What if there were a way to get a pile of money that you don’t owe taxes on? Enter the cash out refinance.

What is a Cash out Refi?

When you refinance a mortgage, you are signing up for a new loan that will replace your old one.

If the amount you own on the old mortgage is less than the new loan balance, you can keep the rest. Since you are turning equity into cash, it is called a cash out refinance.

You might wonder, why isn’t this taxed?

Well you aren’t actually gaining anything – you are turning one asset (equity) into another (cash), while your loan balance increases. Net it is a wash.

Or put another way, you aren’t taxed on money you receive on a loan. In fact, since this is a mortgage, you might even get tax benefit with a mortgage interest deduction!

Rental Property Example with Numbers

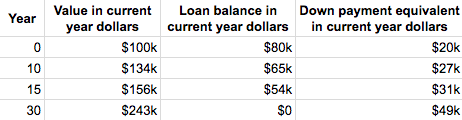

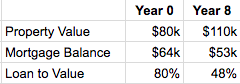

Eight years ago you went through the slight hassle of purchasing a rental property.

The purchase price was $80k and you put 20% down, so your initial mortgage was $64k.

Then it was smooth sailing. The tenant paid the mortgage for you, while you went about your life.

Today the mortgage balance is $53k.

The value of the property also increased to $110k. You were expecting about 3% a year appreciation, keeping pace with inflation, but you got a little lucky with 4%.

Pretty solid build up over 8 years! As a percentage, the loan is 48% of the value of the property.

You have a lot of equity in the property, but that equity doesn’t earn any extra return. Wouldn’t it be great to put that money to work?

The Numbers After a Cash Out Refi

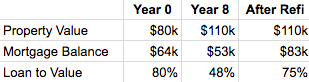

Current rules allow for a 75% loan to value ratio on a cash out refinance.

So you would be starting a new 30 year mortgage with an $83k balance.

You get a new loan for $83k and you owe $53k on the original loan. So you pocket $30k minus the costs of doing the refi, which may be around $4k.

$26k tax free!

Your mortgage payment will go up slightly, but if you have been able to successfully raise the rents, the tenant will still pay it. You wouldn’t do a cash out refinance unless you can still get monthly cashflow on the property.

How to Spend the Money?

You could go on a huge shopping spree, but I like to think of my rentals as a portfolio. I reinvest the earnings from cashflow and equity.

If your property is $110k, I bet others in the neighborhood are $110k too.

If you put 20% down on a new property with $4k in closing costs, it comes to exactly $26k out of pocket. That number sure sounds familiar…

You took the equity from property 1 and used it to get property 2. The first property cloned itself.

In the short term, your net worth suffered as a result of the $4k refi and $4k in closing costs for the new property. But how do things stand in the long run? Well! To begin, you should thoroughly understand any additional costs – closing costs – you may have to bear while dealing with a property by visiting websites such as https://sharonsteelerealestate.com/nj-closing-costs/. This is because it can have an impact on both your short and long-term financial management. When you are aware of all possible outcomes, you can make better decisions.

Projecting Into the Future

Now you are the proud owner of two rental properties. Ballin’!

With the impressive returns on rental properties, what can you conservatively predict?

Each year, for each property:

- $1k in cashflow after all expenses

- $3.5k in appreciation (roughly 3% a year, same as inflation)

- $1.5k decrease in the mortgage balance the tenant kindly pays for you

- Plus tax savings we won’t include here to keep it simple

- Sign up for the email list for the complete breakdown of these numbers

With two properties your overall return is $12k a year. You doubled the amount you earn each year!

Since the second property didn’t require any additional investment, your portfolio only required the $20k eight years ago ($16k down, $4k in closing costs).

Put another way – eight years ago you paid $20k and now your net worth goes up $12k every year!

Do you see how powerful this is?

Starting This Process with My First Rental

I’m currently talking to lenders about a cash out refinance on my Atlanta rental. It has only been 6 years, but my calculations indicate now is a good time.

I’ll share the complete numbers soon, but they are fairly similar to the example above.

When I’ve written about this topic before, people have objected to paying $4k in refi costs to get $26k back. That is a whopping 15% fee!

In my opinion this is stingy – who cares what someone else makes money off me as long as I get mine? This is a win-win situation.

It is also short term thinking – yes there is a hit to your net worth, but you have doubled your earning potential! Project a decade in the future and the right decision is obvious.

I want to hear what you think. Is the fee too much for the tax free lump of cash in a cash out refinance? Do the benefits outweigh the costs?