Can you ever have too much of a good thing?

Yes – doughnut holes. Once you have more than 10, you run out of fingers to put them on. Somehow they don’t taste as good after that…

What about cash flow? Can you ever have too much money flowing into your bank account?

This is what dividend stock investors are chasing. Allow me to set the record straight – there is a better way.

The Appeal of Dividend Paying Stocks

First, what is a dividend stock? It is one that actually pays it’s shareholders a fraction of the profits each year. What a novel concept!

Let’s imagine a company – Beagle Inc. Their shares cost $100 each and you buy one.

Beagle is a great company that turns a profit every year. However, they aren’t in an industry where reinvesting the profits back into the company will produce even better results in the long run. So rather than scaling up, they decide to pay a portion of the profits as a dividend to the share holders. Typically this runs in the 2 to 3 percent range per year.

So at the end of the year, your 1 share of Beagle Inc pays you $2.

Not bad! Most dividend investors will reinvest this back into the company or dividend index fund (yes, you can group together tons of companies that pay dividends) to purchase another fraction of a share (in this case 1/50th).

The following year you own 1.02 shares and earn a larger dividend payout. Fast forward a couple decades and with the power of compound interest, you receive larger and larger payments.

Over time investors hope that the stock price rises, the dividend payments slowly increase, and you can start a snowball effect by constantly reinvesting the dividends in new shares.

What’s not to love?

It Could Be Better…

Companies that pay dividends are not going to experience hyper growth. They are usually well established with predictable profit margins. If they saw the opportunity to reinvest their profits to take on a new market, they would.

Therefore, much of the growth of the stock price and dividend payments will be due to inflation. Meaning, if a company like AT&T experiences profit growth, it likely isn’t because they launched some new-fangled product. It’s because as inflation happens, they slowly keep raising prices.

So you have an investment that keeps up with inflation, pays a bit of a cash flow that you can reinvest, and allows you to start a snowball effect of compound interest. Sounds like investing in rental properties!

Rental properties have four advantages though that make them more appealing than dividend stocks.

1. Better Dividends

Most dividend paying stocks will pay out 2 or 3 percent of the share price per year. Of course there are outliers, but they are riskier. You used to be able to get around 5% a year, but that was likely due to times with higher inflation.

How does that compare to rental property investing? Pretty pathetic.

I’ve been earning about 9% cash return per year on my rental properties. This might be a little higher than longer term projections, but it shouldn’t be hard to get above 6% per year.

This is due in large part to #2 and #3.

2. Better Financing

You don’t have to buy a rental property with all cash! You only have to put down 20% of the value of the property and a bank will loan you the rest at a very attractive interest rate. Well, choosing a rental property that can generate good revenue can be a difficult task. This might be the reason why many of the real estate investors tend to hire agents (similar to realtors Lynchburg) who can filter the search process and find good rental properties for them to buy.

That said, what about Stocks? Almost everyone pays the full price up front. You can technically buy on margin, but even then you need 50% and at any point they can decide they want their money back.

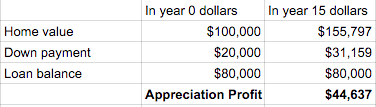

With rental properties you lock in that financing for 30 years.

Most investors don’t understand the power of leverage. A stable rental property in a boring, low-cost city with plenty of jobs will keep up with inflation. Combine that with smart leverage and instead of your investment just keeping up with inflation, you are raking in the big bucks.

3. Better Taxes

Dividend income you have to pay taxes on, even if you immediately reinvest it in more shares. By default this is treated as ordinary income, which means substantial taxes.

However the IRS treats certain dividend investments as qualified dividends. If it’s a US company and you’ve own the shares for at least 60 days, you can usually pay the capital gains rate on those dividends. For me that would mean 15% federal. For the ultra-richies it is 20%.

That’s a pretty nice tax advantage for dividends. But can rental properties top it?

Well, ya! Unfortunately, there isn’t just one number that I can quote you it varies. You get to deduct “phantom expenses” like depreciation. This means you didn’t actually have to pay anything out of your pocket that year, but still get to act as you did on your tax returns. However, make sure to have a separate account for these transactions, so you would be aware of the tax or dividend returns you are getting. If unsure, you can take a look at this list of Best Business Checking Account – Our Top 6 Picks for 2022. It would likely give you an idea about the types of business accounts available for enterprises and you can pick the one best suited for your requirements. This way, you could also find a way to save your taxes.

Moreover, with depreciation alone, most of your cash flow will be tax free! I go into this more in Behind the Numbers – How I Calculated the Return on My Rental Properties.

4. More Control

When you buy a share of stock, you joins millions of other shareholders. Occasionally there might be a shareholder vote, but I think it is safe to say you have zero control.

What if the company decides to go invest heavily in some new market or pay the CEO a $100M bonus? Your only option is to sell your shares.

As a direct investor in rental properties, you run the show. You can reinvest the cash flow, just as you would with dividends, but there are also many more knobs and levers you can use.

One powerful strategy is the cash out refinance – over the years as you build up equity, you can refinance your loan to access the equity tax-free. That’s right, you can receive tens of thousands of dollars, pay zero dollars in tax, and reinvest it in another property (or any other way for that matter). Wow.

You can also “trade up” – selling your property, paying zero in taxes with a 1031 exchange and buying a duplex, four-plex, or apartment building. This is certainly something 1031 exchange brokers can help with!

Maybe remodeling the kitchen would allow you to charge higher rents… think something like that would be possible in dividend investing?

Rentals vs. Dividends

Both are chasing the same thing – cash flow. Yield. Dividends. Whatever you want to call it.

Both allow for the snowball effect of compound interest, which over the course of decades is extremely powerful.

Both are largely dependent upon inflation for growth in the underlying asset, as well as for the cash flow to increase.

But with these four advantages, rental properties clearly win.

What do you think? Should dividend investors consider switching to investing in rental properties?